- Published on

Intensel Whitepaper on Climate Risk and Financial Value-at-Risk Analyses

Resource Link : See ResourceTable of Content

Table of Contents

- Executive Summary

- Conceptual Overview of the Project

- Understanding Climate Risk: A Global and Regional Challenge

- Pricing Climate Risk

- Challenges for Financial Institutions in Managing Climate Risk

- Climate Data and Climate Risk Analytics

- Institutional Capacity Building

- Climate Risk Market Solutions

- Need for an AI-Powered Climatech Solution

- Climate and Financial Valuation Methodology

- Quality of Climate Data and Global Scalability

- Speed of Analysis

- Design of the PoC Platform

- Understanding Current Practices, Solutions, and Gaps

- Current Practices and Tools

- Current Approach to Climate Risk Management

- Gaps and Next Steps

- Applying Climate Risk Analyses on Real Estate Portfolios in Asia

- Capacity Building and Climate Risk Integration

- Results of the PoC in Pricing Current and Future Climate Risk

- Climate Hazard Analysis

- CVaR (Financial Impact) Analysis

- PoC Insights and Next Steps

- Summary

Executive Summary

The increase in major climatic events around the world is resulting in significant damage and financial loss to real assets, from public infrastructure to commercial urban and rural real estate. This is particularly true in Asia, where the impacts from a changing climate are disproportionately more severe than other regions.

Accurately pricing climate risk and integrating this assessment within broader risk management frameworks is a challenge that all financial institutions (‘FIs’) must swiftly address to protect capital and build more climate resilient portfolios.

To address this challenge, financial institutions require better climate data and analytics, education on climate risk, and innovative climate fintech solutions.

This Proof-of-Concept (‘PoC’) project aims to explore solutions to this critical challenge. Working in partnership with ING Bank N.V., Singapore Branch (‘ING’), Intensel Limited (‘Intensel’), a leading Asia-based climate fintech solution provider, conducted a comprehensive climate risk assessment of ING’s real estate portfolio in Asia, and conducted several climate risk workshops to build capacity within the bank.

The climate risk assessment was conducted at a portfolio and individual building asset level. The analysis, which considered future climate scenarios over multiple time horizons, mapped future climate hazard exposure, and converted these findings into financial value-at-risk. Extreme heat, typhoons, and flooding were determined to be the most material climate hazards within the portfolio. Within a portfolio of 136 ‘sample’ assets across 8 markets, the top 10 assets by financial loss make up 62% of the total expected portfolio loss in 2050 due to climate change.

To minimize the inherent risks and to build more climate-resilient portfolios, the PoC confirmed the need for financial institutions in Singapore and globally to acquire more granular climate data, in combination with climate risk-related financial valuation methodologies comparable across geographic markets. Given the number and diversity of assets within financial institutions’ portfolios, climate fintech market solutions will be required to meet the required scale and speed of analyses.

Going forward, financial institutions will be required to integrate climate risk analyses within credit risk ratings and ensure that real estate portfolios sufficiently account for the impact of a changing climate on future valuation models.

Conceptual Overview of the Project

After more than 10,000 years of relative stability, the Earth’s climate is changing, and Asia is particularly vulnerable to the change. Climate science informs us that, without significant adaptation and mitigation, the climate hazards expected to be experienced in Asia in the future, from heat waves to extreme flooding, are likely to be more severe and more intense.

The increase in major climate events results in significant damage and financial loss to real assets, from public infrastructure to commercial urban and rural real estate. As a result, and in addition to the environmental, social, and economic impact on livelihoods around the World, there is an associated instability in capital markets through unmeasured and undisclosed climate risk.

Understanding Climate Risk: A Global and Regional Challenge

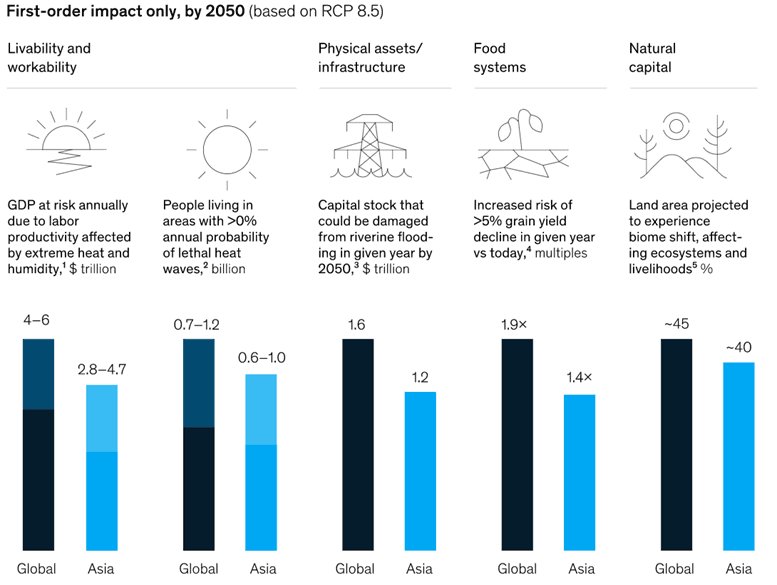

Relative to other parts of the world, the impacts from physical climate risk in Asia could be disproportionately more severe (see Table A) creating greater instability in the economy and increasing the vulnerability of communities. As Asia seeks to grow its economy and ensure stable social development, physical climate risk is thus a critical challenge that the region will need to manage.

Table A: Source McKinsey - Climate Risk and Response (2020)

On the flip side, Asia may be well positioned to address the expected challenges and capture the opportunities that come from managing climate risk effectively. With infrastructure and urban areas still being developed in many parts of Asia, the region can invest in a built environment that is more resilient and better able to withstand higher degrees of physical climate risk. This will provide greater stability for the economy and ensure safer communities.

To do so, however, more accurate and granular climate data and analytics is required.

For Singapore, this presents a unique opportunity to harness its innovative spirit, knowledge, networks, and talent to lead a global response to climate risk that is informed by sound analytics and long-term investment that considers anticipated climate changes. Providing the market with climate risk tools and solutions, based on more robust climate data and analytics, will be critical.

Pricing Climate Risk

Due to the visible increase in the severity, frequency and most importantly the increasing variability of climate hazards, financial losses are growing. This is highly correlated with dense population, rapid urbanization, the growing middle class, and infrastructure build-up in Asia.

According to a McKinsey 2020 report on Climate Risk Response in Asia, “by 2050, under RCP 8.5 scenario, some 7 to 13 per cent of GDP in Frontier Asia and Emerging (ex-China) Asia could be at risk. This compares to 0.6 to 0.7 percent for Advanced Asia (JP, AUS, NZ, SK)”. Severe typhoons and extreme events with 1:100-year probability (=1%) will happen three times more often for countries around the Asia-Pacific region. From the socioeconomic dimension, by 2050 in Asia alone, 600milion-1billion people will experience lethal heatwaves that would cost US$2.8-4.5trillion loss due to reduced outdoor working hours. The list goes on, as does the economic losses and the impact on society.

Given the extent of these identified physical climate risks, regulators are moving to regulate markets to ensure more climate resilient capital markets. Specifically, regulators around the world, including those in Singapore, Hong Kong, and elsewhere in Asia, are moving toward mandatory disclosure on climate-related financial dollar losses.

The TCFD (Task Force on Climate-related Financial Disclosures) and NGFS (Network for Greening the Financial System) have strongly pushed the climate risk disclosure agenda. In most Asia markets, by 2025 major companies and institutions will have to disclose their climate-related risks in line with a globally accepted framework, such as the TCFD. In practice, this currently means mapping and disclosing portfolio and asset-level climate hazard exposure and vulnerability. The ultimate aim, however, is to take the next step by calculating and disclosing financial exposure to current and future climate changes.

Accurately pricing climate risk and integrating this assessment within broader risk management frameworks is a challenge that all financial institutions must swiftly address to protect capital and build more climate-resilient portfolios.

Challenges for Financial Institutions in Managing Climate Risk

The imminent challenge that this is creating for financial institutions is three-fold.

Climate Data and Climate Risk Analytics

Global climate data is in its nascent stages. To make matters worse, datasets in Asia are more patchy and less readily accessible than in other parts of the world. This presents a major challenge in accurately pricing future risk to the extent necessary to make short, medium, and long-term investment decisions.

Institutional Capacity Building

Climate science is relatively new to most sectors of the economy, including the financial sector. Identifying typhoon patterns, and projecting 2030 and 2050-related climate losses, for example, is currently not an area of expertise within the industry. This gap in understanding and institutional capability highlights a key challenge in managing climate-related risks.

Climate Risk Market Solutions

There are limited user-friendly tools that currently exist in the market to enable financial institutions and other businesses to make sense of the data, price the risk, and convert those insights into action that result in more climate resilient outcomes. This is particularly true in Asia. To do this requires high-quality mapping of climate hazards down to the asset level, using multiple data sets and AI innovation. These models must then be converted into financial value under future-facing climate scenarios.

Need for an AI-Powered Climatech Solution

Financial institutions are now under pressure to understand future climate scenarios and to calculate the financial impact that this will have on current and future portfolio value. Given the global scale and geographic diversity of most portfolios, an innovative AI-powered climatech solution is required.

Intensel is a leading Asia-based climate fintech solution provider that has been providing the market with climate risk analytics since 2019, filling a gap that most financial institutions and large corporations do not possess in-house.

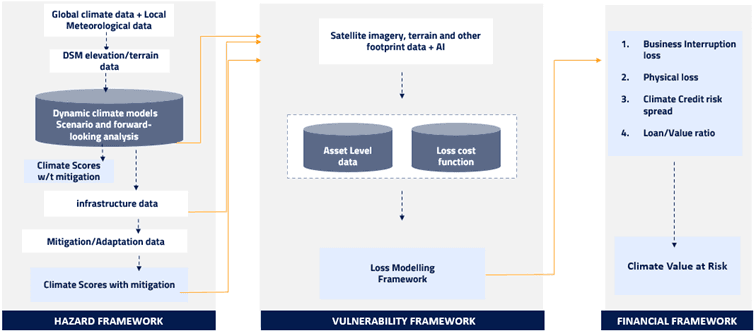

Intensel’s comprehensive solution leverages AI, big data, cloud platforms, supercomputers, and a team of Master’s degree and PhD-level climate and finance experts, to provide financial institutions with a user-friendly climate risk analytics solution. While the Intensel platform details its granular analysis with simple tables, charts, and explanations on a bespoke climate dashboard and portfolio report, the data and technological detail that sits behind the system is complex and multi-layered.

The following chart illustrates the data and technical process of Intensel’s climate risk solution:

To address the challenges that financial institutions are facing, an innovative climate finance methodology, in combination with a unique set of data and analytical expertise, is required.

Climate and Financial Valuation Methodology

In terms of process, the combination of climate hazard data, asset vulnerability analysis through a series of macro-economic data sets, and financial analyses using an insurance approach to calculate financial value-at-risk, creates a unique solution that is rare in the market.

This approach requires multiple different and often unrelated skill sets internally (in terms of human capital), including PhD-level climate scientists and advisors, financial analysts, data security and ESG/climate experts. Intensel is building this unique team and has brought its full suite of capabilities to this project.

Quality of Climate Data and Global Scalability

On the data side, what makes the Intensel solution unique is the quality of the data for Asian markets, which are considered the most challenging geographical locations for climate modelling and financial loss frameworks. From a climate modelling perspective, Asia is exceptionally complex due to excess heat the region receives, making the climate and weather patterns complicated to model. At the same time, the scarcity of regional climate datasets makes financial modelling even more difficult. Intensel has conducted detailed rainfall models for Singapore, for example, and these analytics are built into the Intensel solution.

Intensel takes a unique approach to solving this problem by using models that can assimilate datasets from different sources to model climate with AI/ML. Moreover, Intensel’s model for financial dollar loss uses globally scalable datasets like population, GDP, urbanization, and vulnerability. As a result, Intensel’s model for the world's most challenging region can be extended to other parts of the world with consistently high accuracy. This is important to ensure that Singapore and other Asian-based companies with a global footprint can analyse their portfolios around the world.

Speed of Analysis

The proposed solution leverages AI/ML, which takes input parameters and outputs desired data. These input/output can be packed within a transfer function that stores the data and model's information. The result is that these models take seconds to run instead of hours and days. This feature also makes these models scalable for the cloud in comparison to existing models. Further, these models can be trained on inputs, class, and parameters; hence, the end-user requires minimal or no input or knowledge once the model is configured. In contrast to this approach, existing models require many trained professionals to understand and run models.

Design of the PoC Platform

Given the challenges described above, a comprehensive PoC climate risk analytics project with a leading Financial Institution based in Singapore was developed. The aim of the PoC is to provide insights for Singapore’s financial market and the FI’s that operate within it. The PoC was conducted in partnership with ING, a globally leading FI on matters related to sustainability, sustainable finance and climate risk.

ING takes a holistic approach to climate action. On the one hand, this means acting on how its business impacts climate change, which includes using its Terra approach to steer its loan portfolio towards global climate goals. And on the other hand, this entails considering how climate change impacts its business, as the bank works to assess climate risks and take action to mitigate them.

The PoC was designed to further develop Intensel’s climate models and to refine Intensel’s scalable climate solution to specifically support the requirements of FI’s. At the same time, the PoC set out to inform and educate senior ING decision makers across multiple functions and markets on the complexities of climate risk and financial value-at-risk analyses.

To this end, the project was broken down into two key elements:

- A comprehensive portfolio-level physical climate risk assessment (including the analysis of nine climate hazards) and financial value-at risk analysis for 136 ‘sample’assets across 8 markets within ING’s Asia real estate portfolio.

- Climate risk internal engagement, including multiple meetings and workshops with ING stakeholders (i.e. senior executives) to review the assessment approach, methodology, current climate risk practices at ING, and final results of the PoC analysis.

Understanding Current Practices, Solutions, and Gaps

In its recently published, 2022 Climate Report, ING stated that the company is “making progress” on climate , but still has some work to do. In the 101-page report, ING highlights the work that the financial institution is currently doing to address climate risk, its approach to climate risk management and the areas it still needs to figure out.

These topics were further explored in this PoC. A specific objective was to better understand how FIs approach climate risk integration, and to identify gaps that banks are trying to solve to build more climate resilient portfolios and businesses. The following provides a summary of this analysis.

Current Practices and Tools

ING has already developed a bespoke climate risk identification process that covers both physical and transition risks with respective risk drivers and risk factors. This includes a “climate & environmental risk heatmap”. To do this, the company has assessed the risks for various business sectors based on expert views and external research.

The heatmaps are now being used as input for strategy development and risk appetite analyses for sectors and products in ING’s daily risk management process. This includes incorporating risks indicated by the heatmap in ING’s Sector Credit Risk Appetite Statements (CRAS) to limit the level of credit risk of a sector that ING is willing to undertake. The aim of this practice is to help ING redirect funding from high-risk sectors to those with lower risk and/or green assets.

Up to this point, multiple pilot projects covering sample ING assets in Europe have been conducted with external professional services and data providers for climate hazard mapping and scenario analysis (i.e. RCP 8.5 scenario). Analyses of the implications arising from physical climate hazards for current and future time horizons have been reviewed.

These projects provided ING with initial insights into the impact that a changing climate will have on buildings in general, and specifically on the physical risks that presently exist in its portfolios today, and how this may evolve in the future.

Current Approach to Climate Risk Management

ING’s current assessment is more of a qualitative analysis of climate risk impact. The intention is to increasingly adopt a more quantitative approach, as climate data sets and physical climate risk solutions become more robust.

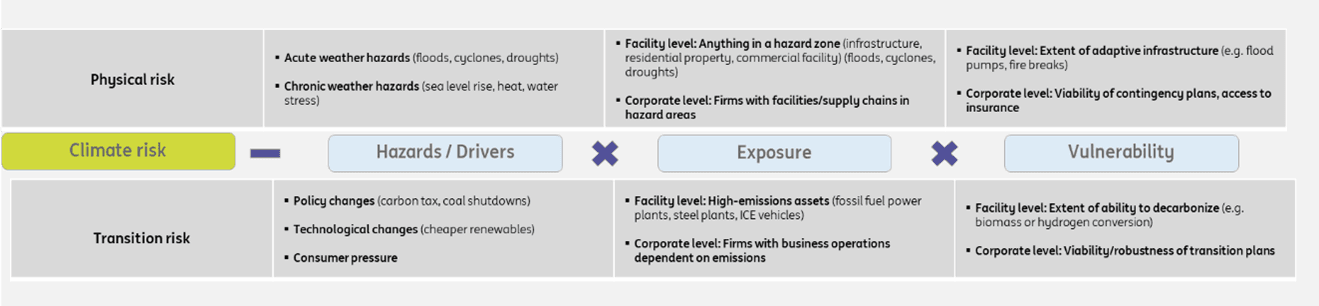

Leaning on global best-in-class methodologies, ING assesses climate hazards, climate asset exposure, and vulnerability for both physical and transition risks. A description of ING’s current approach is articulated as follows:

Gaps and Next Steps

In addition to country level, sector-based, and portfolio-based assessments, ING aims to increase the granularity of its physical climate risk analysis. This includes analyses at the client and individual asset level, which is increasingly what is being required by regulators (i.e. European Central Bank - ECB - Climate Risk Stress Test). In practice, this means moving from assessing physical climate risk at a postal code level to an individual property level to ensure a more accurate risk assessment.

At the same time and linked to the need to assess climate risk at the property level, ING is aiming to further understand the associated financial implications of physical climate risk. This includes translating the impacts of physical climate risk into financial ratios and expected financial losses under multiple climate scenarios and future time horizons. Working with future time horizons can be challenging when it comes to aligning with internal risk frameworks. This is because internal risk management frameworks are typically defined in relatively shorter timeframes (i.e. 3-5 years), whereas climate change assessments look further into the future (i.e. 2030, 2050, and even 2100). In short, while climate change poses long-term challenges, shorter term time horizons are typically used to inform stress tests that are integrated into internal financial risk ratios.

Another challenge that all financial institutions, including ING face, is gathering enough information on asset “vulnerability”. At the asset level, understanding the extent of adaptive infrastructure or processes that have been applied is important to make an accurate financial value-at-risk analysis. At the corporate level, considering the viability of contingency plans and access to insurance, is also an important factor in determining financial value-at-risk. This “vulnerability” data is very challenging to acquire for financial institutions, given the breadth and depth of assets held within portfolios.

Geographic coverage is another gap. As most of the climate risk analyses conducted up to this point in time have been on European portfolios, ING aims to include Asia-Pacific portfolio into its overall global climate risk assessment. As discussed before, quality Asia-Pacific data is challenging to acquire. Furthermore, in the case of multi-market climate risk analyses, the data and methodology applied should ideally be consistent to ensure comparability.

Outside of the access to data, data quality, and methodological challenges faced by ING and other financial institutions, the internal capacity to understand, analyse, and integrate climate risk analyses into existing risk and valuation frameworks is a critical gap to fill in the short term.

Applying Climate Risk Analyses on Real Estate Portfolios in Asia

For this PoC, ING provided Intensel with detailed geographic location information for 136 ‘sample’ real estate assets across 8 markets. This included different real estate asset classes; commercial, industrial, and residential. The PoC included the following:

| Geographical Market | No. Of Properties | Property Type |

|---|---|---|

| Australia | 5 | Commercial / Industrial |

| Mainland China | 84 | Commercial / Industrial |

| Hong Kong | 15 | Industrial |

| Japan | 9 | Commercial/ Industrial / Residential |

| South Korea | 2 | Commercial / Industrial |

| Malaysia | 2 | Industrial |

| New Zealand | 1 | Industrial |

| Singapore | 18 | Commercial / Industrial |

| Total Assets | 136 (in 8 Markets) |

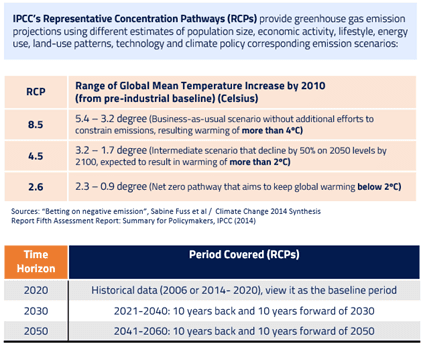

The climate scenarios and time horizons applied to the PoC are defined in the following two tables. Climate scenarios applied were based on the Representative Concentration Pathways (RCPs) set out in the 5th Assessment Report of the Intergovernmental Panel on Climate Change (IPCC), while three-time horizons, including the 2020 “historical data”, served as the baseline period.

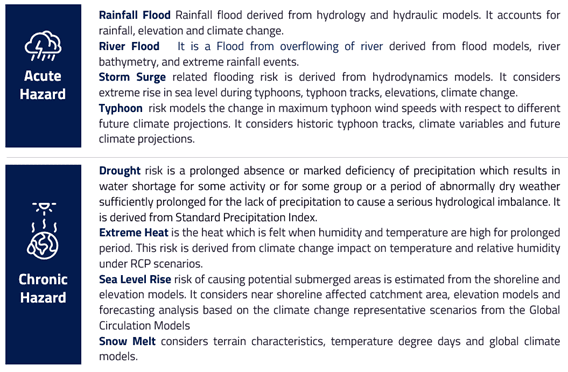

Within the defined climate scenarios and time horizons, the PoC included an assessment of 8 material climate hazards, four of which are defined as ‘acute’ and four of which are defined as ‘chronic’. These hazards align with global frameworks, such as the Taskforce on Climate-related Financial Disclosures (TCFD), and the previously mentioned ECB Climate Risk Stress Test for financial institutions.

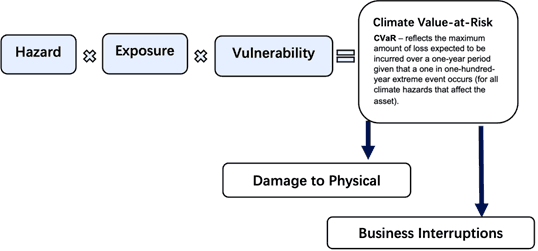

Intensel applied its proprietary climate value-at-risk (CVaR) methodology to the given portfolio. Accurate mapping of climate hazards, the exposure of individual assets to those climate hazards, and the vulnerability of specific real estate asset classes were required to determine CVaR. Within the financial analysis, expected financial losses related to damage to the physical asset itself, plus expected financial losses related to business interruptions were calculated.

Capacity Building and Climate Risk Integration

An important element of the PoC was internal capacity building. As a result, two workshops with ING’s Singapore-based colleagues and global ESG & climate risk team members in Europe were held throughout the PoC period.

Workshop #1 was held on 11 October 2022 and covered broad topics relating to climate risk analyses, including methodologies and financial analysis. This workshop was an interactive session that Intensel developed in partnership with ING to understand how ING currently addresses climate risk within the bank and to understand the barriers that ING face in quantifying the financial value-at-risk resulting from a changing climate. Intensel shared a session on best-in-class climate risk analytics methodologies and how Intensel models climate risk and converts this into financial value-at-risk.

Participants for Workshop #1 included: 7 ING teams from 4 offices (Singapore/Hong Kong/Brussels/Amsterdam), representing the Sustainable Finance Team, the ESG Team, the Global Sustainability “Climate Risk Initiative” Team, and the Corporate Lending Team, the Asia-Pacific Real Estate Finance Team, the Infrastructure Finance and Advisory Team, and the Fintech Team, in addition to the Intensel Team.

A second climate risk workshop (Workshop #2) was held on 16 November 2022. This session included a deeper sharing of banking challenges around climate risk analyses. Intensel also completed its project climate risk analysis and shared the results with the ING teams. A discussion on how to apply the results to credit ratings and other banking metrics was explored.

Participants for Workshop #2 included: 8 ING teams from 5 offices (Singapore/ Hong Kong/Australia/Philippines/Amsterdam), representing the Sustainable Finance Team, the ESG Team, the Global Sustainability “Climate Risk Initiative” Team, the Corporate Lending Team, the Wholesale Banking Team, the Real Estate Finance Team, the Utilities & Infrastructure Finance Team, and the Fintech Team, in addition to the Intensel Team.

Results of the PoC in Pricing Current and Future Climate Risk

While the analysis of the sample real estate assets in Asia Pacific included three future climate scenarios (RCP 2.6, 4.5, and 8.5), the workshop discussions centered on the results from RCP 8.5, given this is the worst-case scenario that results in greatest portfolio risk (and financial loss).

A high-level summary of the analysis results are as follows. Summary charts in this section highlight results from the year 2050.

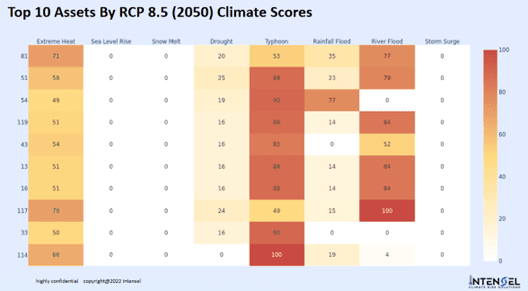

Climate Hazard Analysis

Typhoons and extreme heat were the most material risks for the portfolio of assets, with a “Medium-High”risk factor. Approximately 90% of the assets will be exposed to extreme heat, which will impact energy consumption (i.e. increased energy costs and carbon emissions) in the buildings over time. At the same time, despite the portfolio’s market diversity, based on geographic locations, approximately 80% of the assets have typhoon risk.

Other climate hazards to be aware of include two types of flood risk. Specifically, 34% of the assets (located in Singapore, Malaysia, Australia, Hong Kong, and China) are exposed to increased rainfall flooding, and 29% of the assets (located in Australia and China) are exposed to river flooding. Flooding can be particularly problematic and costly for real estate assets, but can be mitigated with appropriate building flood protection (i.e. flood walls), and effective drainage.

No storm surge or sea level rise risks were identified within the portfolio of assets.

Data analytics are presented in the form of a climate score “heat map”, which visually identifies which hazards are most material. The top ten assets calculated in terms CVaR are listed on the left (N.B. assets are numbered for anonymity) column, while the climate hazards are identified on the top row.

CVaR (Financial Impact) Analysis

The top 10 assets by financial loss make up a significant portion (62%) of the total portfolio loss in 2050. Interestingly, these 10 assets are all located in China. Conversely, the bottom half of the assets within the portfolio will not create much financial loss for the whole portfolio.

It is valuable for ING to be able to quantify expected financial losses at the asset level, as this provides an opportunity to prioritize which assets should be considered first for mitigation measures. This can inform ING’s active engagement focus to build a more resilient Asia-Pacific real estate portfolio.

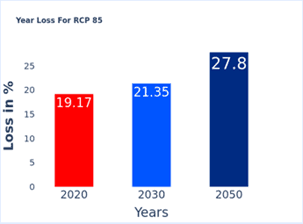

The CVaR in percentage terms (rather than absolute dollar terms) is projected at 21% by 2030 and 28% by 2050 for the portfolio’s total exposure. This translates to approximately 1.6 times the present day CVaR by 2030, and approximately 2.0 times CVaR increase relative to the expected present-day losses by 2050.

River flooding, typhoons, and rainfall flooding are expected to cause the highest losses, which is consistent in global findings. Despite extreme heat having a relatively higher risk score, associated financial losses are relatively small. In addition, it was determined that most of the financial loss would be expected to arise from physical damage to the asset itself, while associated operational losses account for just 1% of the total loss.

PoC Insights and Next Steps

The PoC confirmed the imperative for banks to acquire more granular, accurate climate data and analysis. While regional and district-level climate data can indicate trends, it is insufficient to price climate risk within real estate and infrastructure portfolios.

Climate vulnerability data (i.e. mitigative measures, insurance, etc.) will continue to be challenging for banks and other financial institutions to acquire given the size of portfolios, therefore, having an ability to rank and prioritize assets with respect to climate risk is invaluable. Once a list of top assets is identified in terms of climate risk exposure and expected losses, those assets can be pinpointed to run deeper climate hazard analyses on relevant hazards and to invest time into securing asset vulnerability information. Given the disproportionate loss amounts for a relatively small number of assets within the portfolio, building a more climate-resilient portfolio can be efficiently actioned.

Geographic insight into climate risk exposure can also be useful in building more climate resilient portfolios over time. Specifically, with comparative data and analyses on CVaR per market, banks can enhance due diligence on asset acquisition and de-risk portfolios with internal policies on climate risk that, for example, set lending limits in certain high-risk regions.

In workshop discussions, it was noted that banks in Asia have not yet observed many external real estate valuation consultants incorporating climate risk into property valuations in Asia. This is a significant risk, particularly given the potentially steep rise in future losses for certain assets. While this is beginning to change in markets like Australia, where some valuation reports now integrate the potential financial impacts of sea level rise, forward-looking analyses of physical climate risk impacting asset values are still lacking.

An important area of exploration for banks going forward will be the integration of climate risk into credit risk scores.

While typical loan tenures might not be longer than 5 years, the forward-looking nature of physical climate risk assessments should still be considered in credit risk analyses and asset valuations. This is a nascent area, but the integration of climate risk into credit risk ratings will be a priority in the coming 1-2 years.

In addition to credit risk, forward-looking scenario analysis for climate risk can influence the pricing of loans. In the second workshop of the PoC, many ideas were generated on how to potentially price loans while taking into account a pre-determined climate risk score. This included incentives, such as “climate resilience credits” to encourage mitigation work or setting premiums for selected assets in high-risk locations.

Overall, ING is looking at how to best integrate climate risk into all facets of its risk management processes, and product pricing. Internally, this translates into prioritizing its internal climate modelling and global capacity building over the coming two years.

Summary

Climate risk is an emerging field, and the necessary tools need to be developed to assess the financial risks related to climate change. Despite the heavy technology and terabytes of data involved, these tools need to be easy-to-use. They must also be transparent for companies to understand the financial implications of climate risk so that appropriate mitigative measures can be taken. At the same time, a climate risk assessment should not be seen as a forecast or prediction of risks, but rather as a set of possible outcomes assuming a wide range of climate pathways that are to a certain extent influenced by human, economic, and financial activity.

The results generated in this joint work clearly demonstrated how climate risk manifests for large FIs with inter and intra-regional presence. The analysis can help FIs identify and focus on the core assets that are most exposed to climate change, and then help quantify the risk and compare how these risks differ from the past. These analytics are crucial for risk management and overall better-informed investment and management decisions. Without mentioning climate opportunities, a simple risk reduction strategy can lead to a loss avoidance that can range from 1-10% of the portfolio exposure.